Rock, Paper, Scissors

By Eric Meliton

How has the North American economic slowdown affected the water & wastewater market for the pulp & paper industry?

You might say the pulp & paper industry is between a rock and a sharp place. As the industry faces a downward spiral, market participants struggle to bounce back. From paper manufacturers to equipment suppliers, it has been in a cyclical downturn that has heightened in recent months due to swelling of global inventories, combined with increasing operational costs. Several North American plants, and various global plants, have been forced to cease operation or reduce production output.

According to the Conference Board of Canada, for example, the paper products industry suffered a loss of about $435 million in 2008 – a direct impact on the once thriving water and wastewater services and equipment industries. Indirectly affected by the declining marketplace, core vendors to this industry seek ways to survive.

Pulp & paper industry costs also are increasing for operational and regulatory compliance, while an overall decrease in spending has pinched areas such as capital expenditure budgets and operational forecasts, negatively affecting the overall outlook of all facets of the industry. According to Frost & Sullivan, the water and wastewater industry – inclusive of turnkey solutions, equipment vendors, and operation and maintenance (O&M) services – was experiencing a conservative downturn in 2008, but the overall decline in short-term growth leading into potential decline in long-term growth wasn’t entirely anticipated.

Similar to other manufacturing-based industries, recovery isn’t expected in North America until 2010 at the earliest. Several regions that rely heavily on the pulp & paper sector, expect to be hit the hardest with the current economic strife. North American production is projected to decline as many producers have moved to regions such as Latin America and Asia for more cost-effective operations. As an increased number of North American plants close, a further drop in regional demand for pulp & paper products will likely occur and may continue to slide as 2009 progresses. Another example from the Conference Board of Canada estimates that 2008 production declined by 6.6% and projects that slide to continue on the same pace – resulting in a project loss of business totaling $329 million in 2009.

Withstanding Economic Slowdown

An area in which recovery may be linked is the chemicals sector relevant to pulp & paper manufacturing. Growth is anticipated in pulping chemicals, bleaching chemicals, papermaking chemicals, and specialty chemical products. Despite the slowdown and reduced demand, many of these chemicals experienced higher prices leading into 2009. This trend points to an opportunity for industrial water and wastewater services to create a strategic position beside treatment of these chemicals in the water supply. Another potential area of growth is the tissue sub-segment of the pulp & paper industry. This segment is expected to see the least impact from the economic downturn, which bodes well for relevant technology and treatment suppliers that specialize in water treatment for this niche sector.

Despite declining production rates and closures of key manufacturing facilities, the impact of effluent discharge fines related to regulatory compliance is still considered a major driver in the pulp & paper industry. Reducing the impact of these chemicals on the water supply during production, or as part of the manufacturing process, is still a major concern for facilities. The main drawback at this point is the lack of capital spending available to address these major regulatory concerns.

As this current economic downturn is viewed as a time for precautionary spending, many firms will be unwilling or unable to obtain the necessary credit funding required to upgrade treatment equipment or venture into turnkey or O&M type services. This holds true for water and wastewater treatment facilities affected by industrial water discharges from pulp & paper facilities as operational budgets shrink and smaller communities are strapped for ways to generate private or public funding. If the financial credit crisis affecting major lending facilities and institutions can be alleviated, the industrial sector will benefit as a whole with increased access to credit and financial funding. Major overhaul projects won’t be put on hold, and facility upgrades on both the utility side and industrial sector will benefit.

The economic downturn will continue to impact the North American pulp & paper industry, however, if major manufacturers are expected to shut down facilities or cut rates of production. As of early 2009, manufacturers such as Domtar, Metso Paper, Abitibi Bowater, and Voith Paper each announced facility closures and reduction in operational capacity at North American facilities. This has resulted in many job losses and an indirect impact to the water treatment sector.

Despite these projected job losses and facility closures, O&M in all facets of the pulp & paper industry have the largest long-term potential for recovery and growth. Not only are facilities seeking such services for water and wastewater treatment, but this service-driven deliverable has also extended into manufacturing and production capabilities. Firms that can customize services beyond just water applications could capture more market share as manufacturers seek ways to maximize operational budgets, while reducing overhead and inefficiencies.

What Does the Future Hold?

Despite being one of the largest consumers of pulp & paper, North America will continue to experience a decline in this industry. Even so, regional pulp & paper production will remain one of the largest industrial consumers of freshwater and energy to maintain standard manufacturing practices.

Continued demand to address compliance issues related to wastewater treatment and sludge disposal methodology will still be relatively high as both North American and global water shortages become more relevant. For every ton of pulp production, about 17,000 gallons of industrial process water is required. Technological advances into sludge dewatering equipment or enhanced wastewater treatment will become leading opportunities for industry vendors in this sector. Inexpensive ways to enhance treatment, such as top-of-the line aeration equipment, could become a simple, yet robust solution for both utilities and industrial manufacturers.

Manufacturers have already addressed some of the long-term issues affecting the industry. The focus of the sector has been toward inward improvement. Many manufacturers are reducing air emissions, water footprint, and rethinking products that rely heavily on chlorine and other chemicals for bleaching and pulping processes. Having manufacturers see the benefits of these improvements to manufacturing paradigms will positively impact the water and wastewater industry – making it easier for new technology advancements or process improvements to take hold.

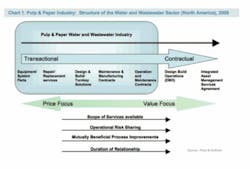

Chart 1 depicts the current market structure of the water and wastewater industry in the pulp & paper industrial sector. As shown by the diagram, there’s a shift from strictly transactional equipment market opportunities to more contract-based opportunities for different firms. Firms that can offer added value industrial services will be able to maintain a strong market presence, despite the current struggle of the pulp & paper industry. Long-term positioning in anticipation of this perceived shift in the current market structure will assist firms that can address more flexible needs for the industry.

Existing Industry Opportunities

Freshwater conservation is still considered one of the major stewardship trends for the pulp & paper industry, and it’s a top initiative for many manufacturers. Since water is imperative in all major stages of pulp & paper production (average mills utilize 63 million liters of freshwater per day for production and wastewater needs), regulatory compliance combined with increasing freshwater rates will continue to drive industry participants to find improvements for both water treatment and water conservation technology. Currently, freshwater costs represent about 10% of overall industry production costs – a figure that’s expected to decrease as firms make major improvements in the near future.

Retrieval of contaminated wastewater, i.e., treated for reuse, is a unique opportunity within the industry that has yet to be maximized. About 85% of water used in the pulp & paper industry is composed of wastewater that’s contaminated with effluent solids, absorbable organic halides, chemical and oxygen demand sediments, and chlorinated organic compounds.

In addition, another opportunity that exists for the water and wastewater sector includes more efficient treatment of sludge generated by the pulp & paper industry. Sludge drying and dewatering technology can improve costs associated with transportation, dumping or storage, and relative tipping fees that are charged based on tonnage. Technology to improve drying capabilities even in small percentages can result in millions of dollars saved each year in these fees. Although there are no major firms leading in this specific technological advancement, many smaller firms may offer technology to address the issue. Continuous sludge processing improvement may positively affect the overall burden of tipping fees and result in a boom in dewatering equipment utilized by this industry. Similar applications of this technology can already be applied to the chemical manufacturing, pharmaceutical, and food & beverage sectors – all major producers of sludge and with major expenditures related to tipping fees.

About the Author: Eric Meliton is a senior research analyst with the Palo Alto, CA-based global growth consulting company Frost & Sullivan’s North American Environmental Technologies practice. Before this, he was a quality assurance specialist for the pharmaceutical industry and a chemist for the precious metals industry. Contact: [email protected] or www.frost.com