GE Strikes Again: Last Remaining Membrane Pure-Play Swallowed

Powerhouse General Electric, which has targeted the water industry as a key growth platform, recently dove deeper into the market by acquiring Zenon Environmental, one of the few remaining membrane filtration companies as well as publicly traded “pure-plays” in the water sector.

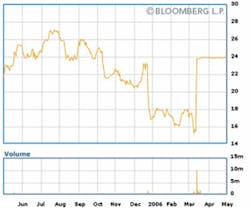

Zenon, formerly a darling on the Toronto exchange, fell over 40% in market value, from C$27 to below C$16, since last July on earnings losses due to manufacturing problems when it upgraded a key product line. The stock had a long bumpy downhill ride, with a series of negative announcements and loss of investor confidence. Despite this, it continued to look expensive as earnings estimates also dropped. Even at its lowest point, Zenon was still trading at a generous 19x analysts’ 2006 EBITDA estimates and over 100x consensus EPS.

Ongoing troubles, it appears, compelled Zenon’s founder and major shareholder Andrew Benedek to negotiate a sale a bit sooner than expected. Based on consensus estimates, GE’s C$24/share takeout price (for C$760 million total, or about US$655 million) represented a 55% premium to its depressed share price and a 30x EBITDA multiple based on ’06 consensus estimates. Even considering the lofty takeout multiples in the water sector (12-18x EBITDA), GE’s offer seemed outlandish at first glance. Still, Zenon’s current profitability is far below potential and, in our view, GE paid a relatively reasonable price for Zenon’s state-of-the-art membrane technology and extraordinary growth opportunities in the sector.

Examining the acquisition on a multiple of sales, GE paid about 3.3x ’05 sales of C$238 million, which were hurt by project delays, and about 2.7x ’06 sales estimates of C$290 million. In our view, Zenon’s technology leadership position in microfiltration and ultrafiltration (MF/UF) membranes combined with GE’s global market presence and manufacturing capabilities should allow top-line growth rates in this specialty platform in the 20-25% range over the next several years. UF membranes, which offer microbial level contaminant removal at prices increasingly competitive with conventional treatment, are taking share in the drinking water market and appear to have even greater upside potential in the wastewater market, where membrane bioreactor (MBR) technology is revolutionizing wastewater treatment, particularly in industrial applications.

With the bulk of its existing $2 billion or so in water group revenues concentrated in industrial water treatment, GE already put a toe in the water of the municipal market with last year’s acquisition of Ionics. The Zenon purchase puts it definitively in the huge municipal water infrastructure market, with a compelling technology position in the higher-growth end of the treatment market. In addition, GE’s project and vendor financing capabilities give it an advantage relative to other participants in the systems market, such as Siemens, ITT Industries, and Pall Corp.

GE also recently replaced its water group chief, appointing Jeff Garwood as new president and CEO of GE Water & Process Technologies. Garwood appears enthusiastic about opportunities he sees ahead. He says no one else has the breadth or scale of capabilities GE has, and he indicated his intent to ramp up GE’s efforts to leverage its product portfolios across a range of end markets. In particular, GE continues to talk about its capability to put together water, power and financing capabilities to develop large combined water/power projects in the Middle East more efficiently than competitors - typically large engineering firms.

Conclusion

We’ll be interested to see if a change in management at GE Water might result in a truce in the price war in water treatment chemicals that last year hurt both Nalco, the largest U.S. water treatment chemicals company, and GE Betz, the second largest. Garwood acknowledges there has been “price compression” in the chemicals business but won’t publicly address his pricing strategy going forward. In year-end results, Nalco said increases in energy and raw materials costs outpaced yearly price increases by about $15 million. We think the pricing environment in this segment could be somewhat less harsh in 2006.

About the Author: Based in Washington, DC, Francesca McCann is a vice president of the Stanford Washington Research Group, a member of the Stanford Financial Group, and a senior research associate for water/transportation markets. The 30-year-old group consistently ranks among the top three in its category in Institutional Investor Magazine.